Welcome to my personal website.

I am Chunjie Wang. I am an assistant professor in finance at KU Leuven. I obtained PhD in finance at Stockholm School of Economics. My research interest lies in empirical asset pricing, and machine learning applications.

You can reach me by my social accounts or by email at chunjie.wang@kuleuven.be

Working Paper

Asset pricing, not equity pricing

job market paper

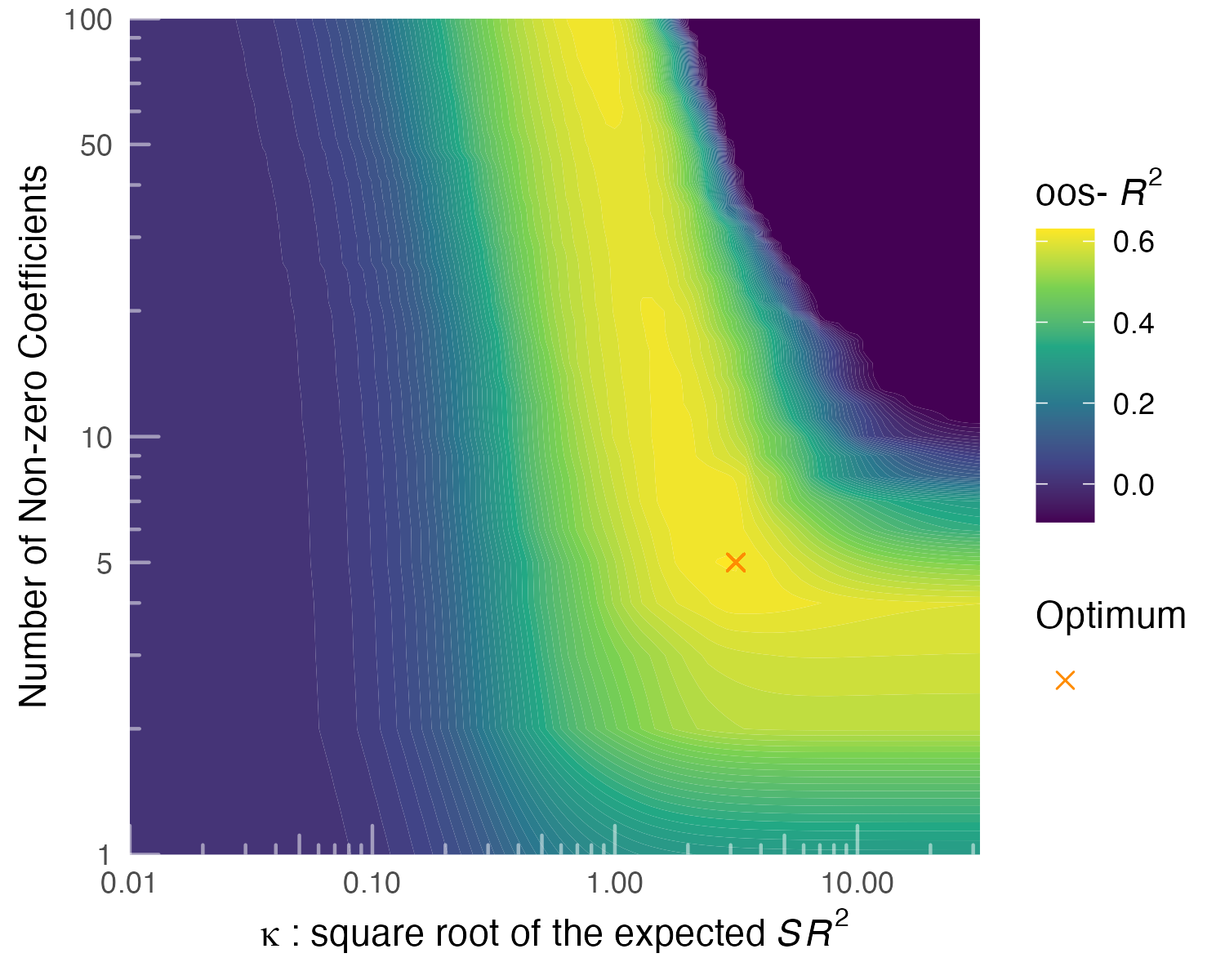

This paper demonstrates that building characteristics-managed factors using firms' asset returns greatly reduces the number of factors necessary to explain the cross-section. A 5-factor model based on asset returns explains 62.4% of the variation in 100 factors, whereas an 88-factor model using equity returns explains only 38.6%. Out-of-sample, the asset-based implied mean-variance-efficient (MVE) portfolio achieves a Sharpe ratio of 1.2, compared with 0.75 for its equity-based counterpart. The parsimonious asset-based model explains equity returns better than the equity-based model, as it reduces the number of equity anomalies to 15 compared with 23 for the latter. The nonlinear transformation of returns caused by leverage increases the loadings of firms with high leverage on the equity-based factors, exposes these factors to firm-level systematic risks that would not arise in asset-based factors, and contributes to the factor zoo.

The Volatility Smile of Expected Returns

with Adrien d’Avernas, Christian Schlag, Tobias Sichert, and Martin Waibel

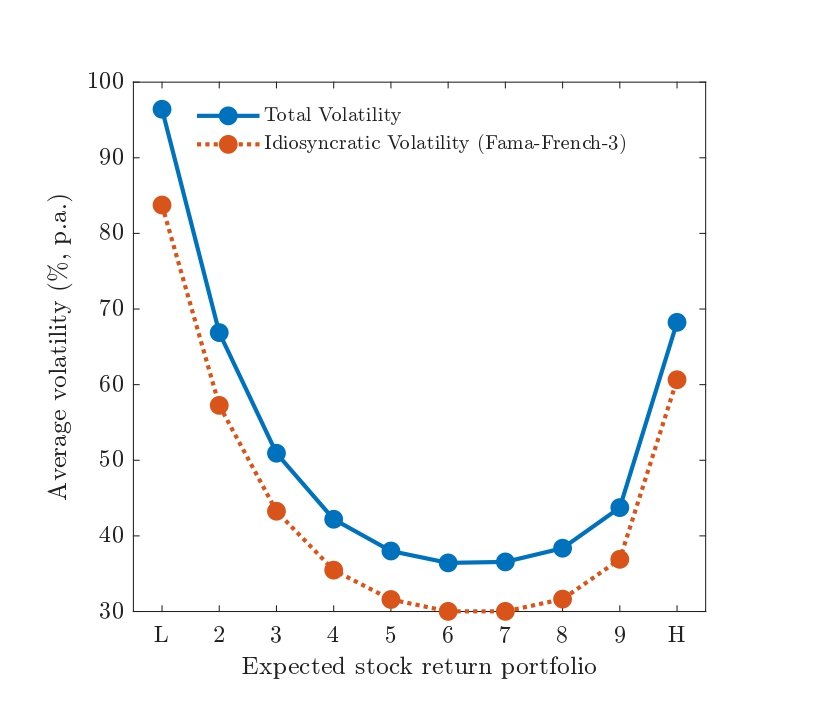

In the cross-section of stocks, expected returns and volatility exhibit a pronounced U-shaped relation: stocks in both tails of the expected-return distribution are substantially more volatile than those in the middle. This fact shapes how risk premia are transmitted across the capital structure. Because volatility enters option and bond elasticities with respect to the underlying with opposite signs, a given expected-return signal is compressed in options but amplified in corporate bonds. The U-shape also explains the empirical fragility of the idiosyncratic-volatility anomaly: the unconditional relation between volatility and expected returns represents a mix of two conditional relations with opposite signs.

Education

Stockholm School of Economics

Stockholm, Sweden